This humanoid robotics company is going public, but its CEO isn’t promising a robot in your home anytime soon

Digital Frontier EditorialJuly 6, 20265 min read

Key Takeaways

Agility Robotics will become the first pure-play humanoid robotics company on public markets via a $2.5 billion SPAC merger, raising $620 million — the sector's largest capital raise to date.

CEO Peggy Johnson refuses to sell the home-robot fantasy, insisting Agility's bipedal Digit stays in warehouses and factories where the economics actually work.

The SPAC structure sidesteps IPO scrutiny but carries stink from 2021's spectacular flameouts; Johnson calls it a timing play, not a desperation move.

Unlike competitors burning billions on R&D with zero revenue, Agility has a 70,000-square-foot factory, a customer pipeline, and a CEO who helped Microsoft buy LinkedIn — then ran Magic Leap into the ground.

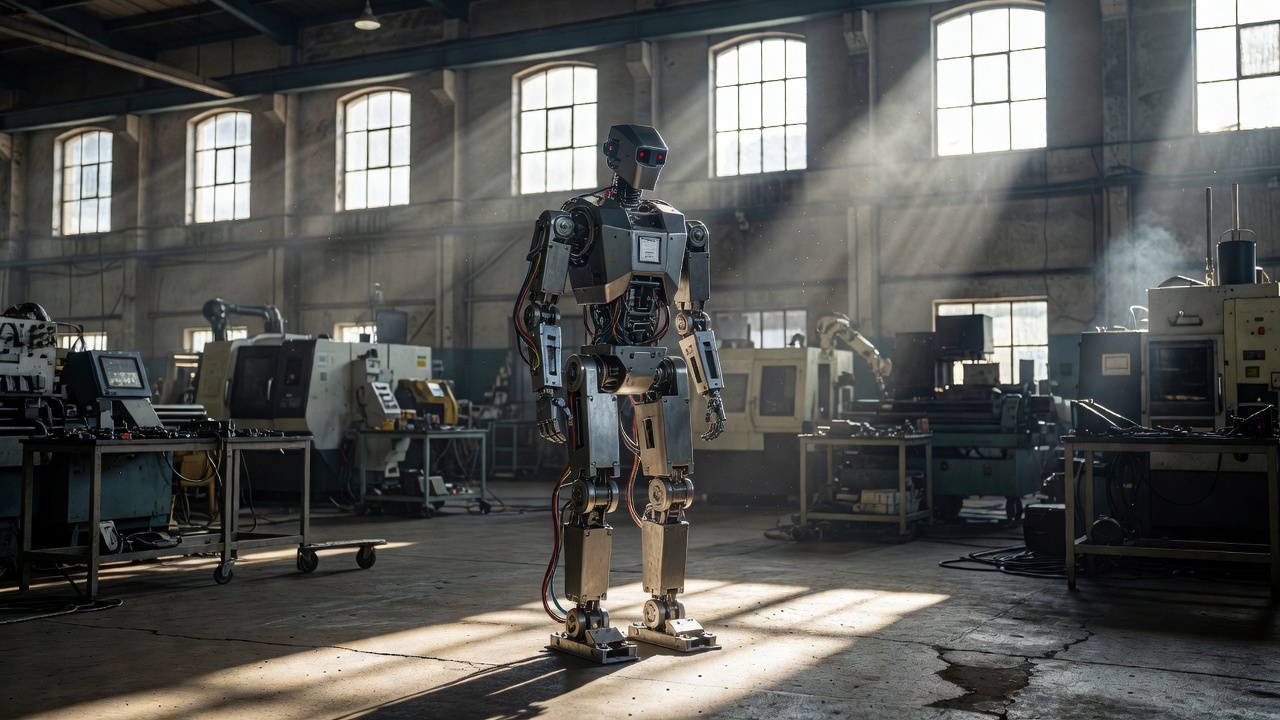

The humanoid robotics gold rush has a new claimant. Agility Robotics, the Salem, Oregon outfit building bipedal warehouse workers, is going public through a SPAC merger that values the company at $2.5 billion. The deal with Churchill Capital Corp XI promises $620 million in gross proceeds — the largest capital raise in the sector's short, cash-incinerating history.

But CEO Peggy Johnson isn't selling the dream.

Ask her when a Digit robot will fold your laundry, and she won't bite. She declines to disclose the bill of materials. She refuses forward guidance. She pushes back, politely but firmly, on any question that smells like hype. This is a woman who orchestrated Microsoft's $26 billion LinkedIn acquisition and later steered Magic Leap — once valued at $6.4 billion — into a quiet sale after the augmented reality hype evaporated. She knows the difference between a market and a mirage.

The money is stupid right now

Figure AI: $39 billion valuation. Apptronik: $5.5 billion. AI2 Robotics: $3 billion. None are public. None have meaningful revenue. All are raising nine-figure rounds on the promise that general-purpose humanoids will soon justify those prices.

Agility's $2.5 billion tag looks almost modest by comparison. But Johnson's SPAC play is a different beast. It forces disclosure. It creates a currency for acquisitions. It hands retail investors a sector bet that has existed only in venture portfolios. And it does so while the SPAC structure itself remains radioactive — a vehicle that enriched sponsors in 2021 while leaving shareholders holding bags of worthless equity.

Johnson knows this. She calls the deal "an acceleration story and a timing story." Translation: we're going public before the music stops.

Warehouses don't care about your sci-fi

Here's what separates Agility from the parade of CGI demos and teleoperated stage props: Digit actually works in production. Amazon tested it. Spanx uses it. GXO Logistics has a deployment agreement. These aren't pilots — they're purchase orders.

The robot doesn't backflip. It doesn't make coffee. It hauls totes from shelf to conveyor belt, 20 hours a day, in facilities built for humans. That's the pitch. Bipedal form factor, human-scale workspace, no infrastructure retrofit. The economics are narrow but legible: replace transient labor in the most miserable tasks, amortize over three shifts, collect recurring revenue.

Johnson won't say what Digit costs to build. She won't say what they charge. But she confirmed a manufacturing facility — 70,000 square feet in Salem — and a pipeline she describes as "substantial." That's more concrete than anything Figure or Apptronik have shown publicly.

The Magic Leap ghost

Johnson's tenure at Magic Leap haunts this narrative. She took the helm in 2020, after the hype cycle peaked and the layoffs began. She sold the company's assets to a consortium of investors in 2023 for a fraction of its peak valuation. The AR revolution never came. The "spatial computing" category she championed dissolved into Apple's Vision Pro and Meta's Quest.

Skeptics will line up to say she's running the same playbook: raise big, promise big, deliver niche. But there's a difference. Magic Leap burned billions developing a consumer platform nobody asked for. Agility builds industrial hardware for a labor shortage that isn't theoretical. U.S. warehouses have 600,000 unfilled jobs. Turnover exceeds 40%. The demographic math is brutal — fewer young workers, more e-commerce volume.

Digit doesn't need to be smart. It needs to be reliable. That's a harder engineering problem than intelligence, but a more soluble business problem.

First mover, first target

Going public first makes Agility the sector's benchmark. Every quarterly report will be parsed for signals about the entire category. Every miss will drag down private valuations. Every disclosure becomes a weapon for competitors who stay private.

The SPAC structure amplifies the risk. Churchill Capital Corp XI is a blank-check company — Michael Klein's eleventh. Sponsors get promote shares at a fraction of the public price. If the stock tanks, they still profit. Retail buyers absorb the downside. Johnson insists the structure was about speed, not avoidance. But the SEC still has to approve. Shareholders still have to vote. The deal isn't done.

And the $620 million? It disappears fast at this burn rate. A 70,000-square-foot factory, a few hundred employees, R&D on the next generation — that's $100 million a year minimum. Three years of runway if nothing goes wrong. In hardware, everything goes wrong.

No home robot. Not soon. Maybe never.

This is the line Johnson draws most sharply. The home is unstructured, unpredictable, full of stairs and pets and toddlers and liability. The unit economics require a price point no consumer will pay and no insurer will underwrite. She's seen this movie. She knows how it ends.

So Agility stays in the warehouse. The SPAC money scales the factory. The public listing creates liquidity for early investors and currency for talent. Johnson bets the company on a narrow, ugly, profitable wedge — and refuses to pretend it's a wedge into the living room.

In a sector drowning in science fiction, that restraint might be the most valuable asset on the cap table. Or it might be the reason the stock trades below the SPAC's $10 floor within twelve months. The market will decide. Johnson has stopped pretending she can control it.